Thailand Health Insurance For Long-Term Visitors

Long-term visitors in Thailand must have private health insurance that fulfills visa requirements and provides reliable protection for medical emergencies. Since foreign residents are not covered by the public healthcare system, having a comprehensive policy is essential for safety and compliance.

Discover the world's top

health insurers.

Compare quotes with

a click of the button.

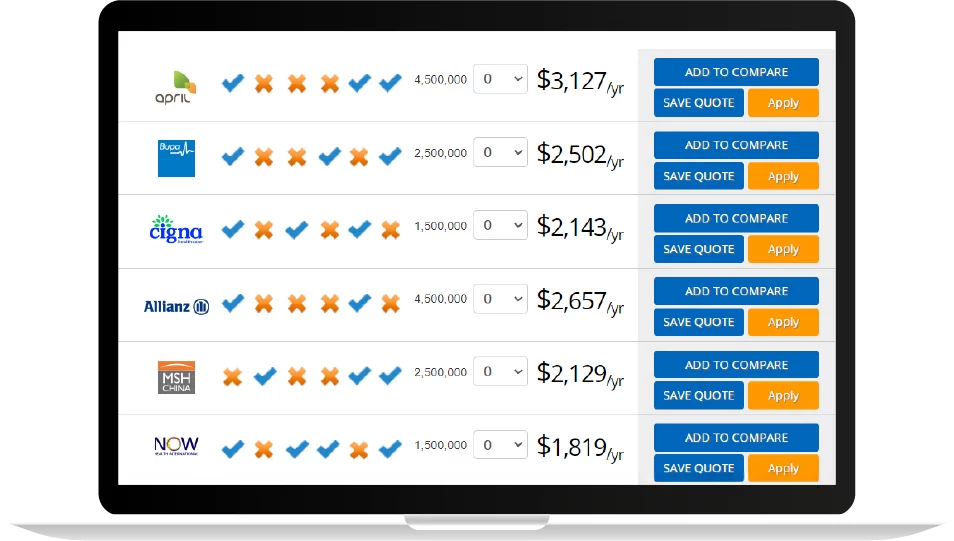

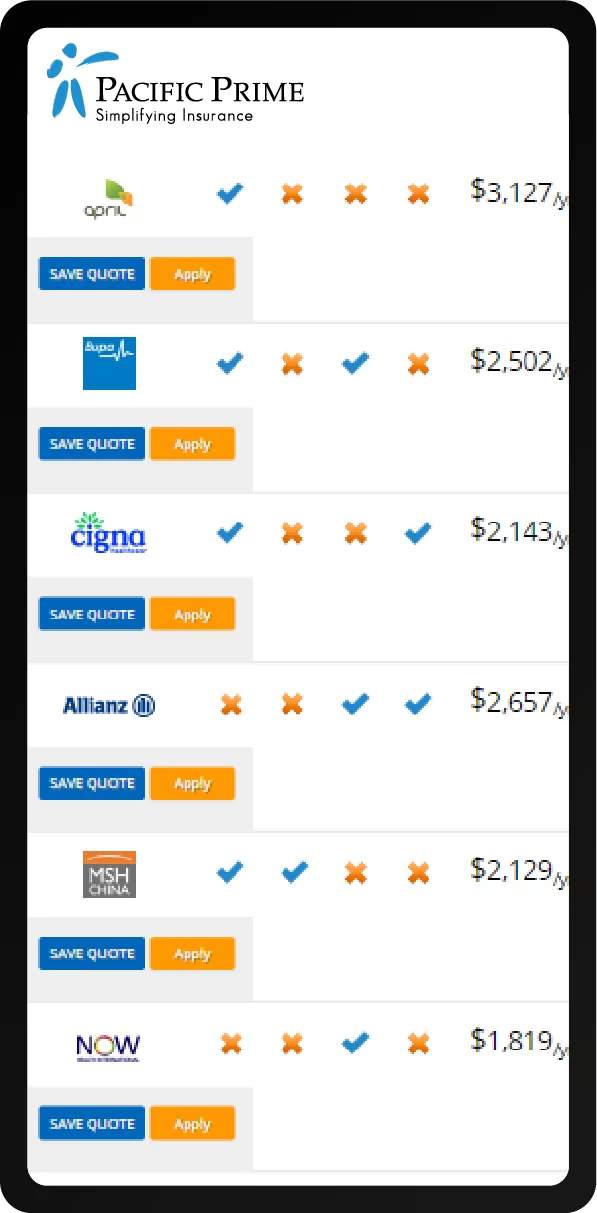

Compare health insurance plans for long-term stays in Thailand. Get a free, no-obligation quote from Pacific Prime and compare plans from leading local and international insurers to find coverage that meets your visa requirements and budget.

Planning to retire, work remotely, or stay long-term in Thailand requires choosing a health insurance plan that meets visa requirements for Non-Immigrant O, O-A, and O-X categories while providing access to quality private hospitals.

This Pacific Prime guide highlights the key features to look for in an expat health insurance plan to help you stay fully covered and worry-free throughout your stay.

Why Private Health Insurance Is Essential for Long-Term Visitors in Thailand

Long-term visitors in Thailand most likely will not qualify for the public health insurance scheme in Thailand, making private health insurance crucial for themselves and their families. Many expats also prefer the extra comfort provided by private insurance. If you are unsure whether this type of coverage is right for your situation, learn more about Do expats need private insurance in Thailand and how private plans can help expats access quality healthcare.

Private health insurance grants you access to the private clinics and hospitals that have state-of-the-art facilities, faculty that speak English, higher levels of care, and access to more equipment.

Each of the following cities has some of the best private hospitals in Thailand:

- Bangkok

- Chiang Mai

- Phuket

- Pattaya

- Koh Samui

- Hua Hin

You’ll want to research each so you can guarantee you live close to the facilities you want to use. It’s more important than ever to find the right location and the right insurance plan with the rising health insurance costs in Thailand.

This article will discuss several factors you want to consider as you choose your health insurance plan, as well as some qualities that make up a strong plan.

Important Factors When Selecting Health Insurance in Thailand

As you choose your health insurance, you will want to consider factors such as expats paying higher costs for treatment than Thai citizens, medical evacuation, and long-stay visas health insurance requirements.

We will discuss each of these factors related to long-term visitor health insurance in Thailand below.

Healthcare Costs for Foreigners in Thailand

Expats, digital nomads, and foreign long-term visitors to Thailand may have to pay almost twice as much for their health treatments as their Thai citizen counterparts dur to dual pricing system in Thai public hospitals.

The dual pricing system breaks people up into three tiers: Thai Citizens & Neighbors, Expats, and Retirees & Tourists. Each tier is charged different fees for the same treatments.

Thai Citizens pay the least, then expats, with Retirees and Tourists paying the most for the exact same treatments.

Why Emergency Evacuation Coverage Matters in Thailand

If you have a medical emergency in rural Thailand, you may need emergency transportation to the nearest facility or country. Rural cities in Thailand have fewer resources and the facilities are of lower quality, so expats will want to have the option to be transported to a hospital with better care.

Make sure you have a health insurance plan with a medical evacuation rider. This will ensure you have coverage to be driven or flown to a hospital with proper equipment, sanitation, and specialists who can treat you in an emergency.

Health Insurance Requirements for Thai Long-Stay Visas

If you’re a long-term visitor to Thailand trying to get a Non-Immigrant Visa Category O, a Non-Immigrant Visa Category O-A, or a Non-Immigrant Visa Category O-X, you are required to have health insurance. If you don’t have sufficient health insurance, you will not qualify to obtain a visa.

Here are the Thai health insurance requirements for long-term visitors:

- Non-Immigrant O (Retiree): Outpatient coverage of no less than THB ฿40,000 (about USD $1,100) and inpatient coverage of no less than THB ฿400,000 (about USD $11,600).

- Non-Immigrant O-A (Long Stay): The Total sum of the insured must be no less than THB ฿3,000,000 (USD $100,000) per policy year, and they must have coverage for COVID-19.

- Non-Immigrant O-X (Long Stay): At least US$ 50,000 (approx. THB 1,609,039) in insurance coverage, or currently receiving social security benefits in Thailand, or having a deposit of at least US$ 100,000 (approx. THB 3,217,842) in a bank account

To guarantee that you can get a visa to move to Thailand, you should look for healthcare plans that will provide you with sufficient coverage for the visa you need.

Learn more about the types of visas in Thailand to determine what types of health insurance, if any, you are specifically required to have.

You’ll also want to become familiar with Thailand’s new requirement that visitors must have health insurance coverage for COVID-19.

Key Benefits to Include in Thai Expat Health Insurance Plans

Long-term visitors to Thailand need strong health insurance plans with qualities such as international coverage, 24/7 customer support, guaranteed renewability, direct billing, inpatient and outpatient coverage, pre-existing conditions coverage, emergency evacuation, and maternity care.

If you are ever unsure if the elements of a health insurance plan are sufficient for your needs, contact an insurance expert to hear their unbiased advice. Getting expat health insurance in Thailand is very important, and should not be a rushed decision.

Comparing different providers can also help you understand your options, so take a look at our guide to the best health insurance companies in Thailand for an overview of leading insurers and available plans. When researching your options, you can also learn more about Luma health insurance Thailand and how its plans may suit the needs of long-term visitors and expats.

Benefits of International Health Coverage for Expats

International health coverage covers your healthcare costs anywhere in the world. It could cover care like emergency treatments, hospitalization, inpatient and outpatient care, vision or dental, maternity care, or repatriation. This is essential for expats who travel regularly.

The Importance of 24/7 Customer Support in Health Plans

When long-term visitors in Thailand or any country have medical or insurance questions, they need to be able to contact their insurance company or broker at any time of the day, any day of the week. Make sure you select a plan that has 24/7 customer support so you can get support at all times.

This is particularly important if you travel often and are constantly switching time zones.

Why Guaranteed Renewability Protects Your Coverage

Guaranteed renewability means the insurance company or broker is required to offer you the chance to renew your plan at the end of your contract, so long as you are continuing to pay your premiums.

This means your health, job, or hobbies can’t affect whether or not you qualify for their insurance. It is a measure of protection for the insured to be able to renew their plan each year.

Advantages of Direct Billing in Thai Health Insurance

Direct billing lets your insurer pay their fees to the medical hospital or clinic directly, only contacting you if there is excess you are required to pay. This is more convenient as it saves time and keeps you from having to pay out of pocket and then filing for reimbursement.

If you don’t have direct billing, you will be required to pay the entire treatment cost to the medical facility out of pocket at your visit. After that, you contact your insurance company to claim back a reimbursement for what your insurer has agreed to cover.

“Pay and claim” plans are not only a hassle for you, but they can be stressful and even impossible if you don’t have enough money in your account to cover the entire cost out of your bank account the day of the visit.

Difference Between Inpatient and Outpatient Coverage

Inpatient coverage is insurance for treatments and procedures done when you are required to stay in the hospital overnight. Outpatient coverage is insurance for treatments and procedures that are done either in a clinic or in the hospital without being admitted overnight.

Below are some lists to better explain the difference between inpatient and outpatient coverage.

Common care inpatient coverage includes:

- Hospitalization

- Surgeries that require an overnight stay

- Tests

- Procedures

- Ambulance expenses

- Medications

- Nurse and Doctor costs

Common care outpatient coverage includes:

- Routine checkups

- Tests

- Procedures

- Surgeries that don’t require staying overnight

- Medications

- Vaccinations

- General Practitioner costs

How Thai Insurers Handle Pre-Existing Condition Coverage

Pre-existing conditions are health issues that existed before your plan begins, such as asthma, diabetes, or chronic illnesses. In Thailand, insurers may sometimes apply loadings (higher premiums) to account for these conditions.

Coverage for pre-existing conditions is reviewed on a case-by-case basis and depends on the insurer’s underwriting guidelines. Our experienced advisors will work with you to secure fair terms on pre-existing cover and guide you toward a plan that best suits your needs.

Maternity and Pregnancy Insurance Options in Thailand

Maternity insurance provides health insurance for all pregnancy-related treatments, such as routine checkups, vaginal deliveries, c-section deliveries, postpartum recovery, and more. When traveling and living abroad while pregnant, you will want to guarantee you have coverage.

You will also want to make sure you are residing in the best places to live in Thailand so you can have close access to the best healthcare facilities.

Dental Coverage and Waiting Periods in Thai Health Plans

Dental coverage under most plans includes comprehensive benefits for both routine and major dental procedures. The minor dental benefits kick in immediately, covering preventive care like regular check-ups, cleanings, polishing, plaque removal, sealants, and other basic treatments.

Certain benefits, such as surgeries, extractions, root canals, and sometimes orthodontic treatment like braces, have a waiting period of around 9-10 months before you can utilize them. This allows the insurer to mitigate risks related to pre-existing conditions.

Once the waiting period is over, you gain access to these crucial major dental services that help maintain your oral health. Thus, it’s advisable to inquire about the specific coverages and waiting periods of your chosen dental plan.

Understanding Medical Evacuation and Repatriation Coverage

Medical evacuation involves transporting a patient to the nearest appropriate medical facility in case of a serious medical emergency. For many expats living in Southeast Asia, Thailand is a common destination for such evacuations due to its advanced medical infrastructure.

Evacuation services are incredibly costly. As a result, insurers have stringent criteria for qualifying individuals for this benefit. Meeting the requirements for medical evacuation coverage is a complex process, given the substantial financial implications for the insurers.

Therefore, all expats should carefully review and understand the evacuation-related terms and conditions in their health insurance policies.

FAQs About Health Insurance in Thailand

How much does it cost to see a doctor in Thailand without insurance?

A GP consultation in a public hospital can be highly affordable, with a cost around THB ฿30-200, depending on the tests and procedures needed. A GP consultation in a private clinic is usually more expensive, at around THB ฿500 to ฿2,000.

Is health insurance mandatory for long-term visitors in Thailand?

Health insurance is mandatory for long-term visitors in Thailand because they need it to meet visa requirements, such as the Non-Immigrant O-A or Long-Term Resident (LTR) Visa.

How much does health insurance cost for long-term visitors in Thailand?

In Thailand, a health insurance plan costs around USD $4,695 on average for an individual health insurance plan and USD $18,027 for a family health insurance plan.

How long can a non-immigrant live in Thailand?

If you are a long-term visitor living in Thailand on a non-immigrant visa O-A, you can live in Thailand for up to one year, so long as you do not work. If you have a non-immigrant visa O-X, you can live in Thailand for up to 10 years, so long as you do not work.

Can tourists buy health insurance in Thailand?

Tourists can purchase travel insurance with health and accident coverage from insurers in Thailand. Insurers like AXA and Allianz have travel plans that are tailored for inbound tourists and expats.

Does the Thai retirement visa require health insurance?

If you are retiring in Thailand with the Non-Immigrant O-A (Long Stay) visa, you’ll need health insurance to comply with the visa. For the Non-Immigrant O (Retirement) visa, insurance is not required but is still strongly recommended.

What is the 30-baht healthcare scheme in Thailand?

The 30-baht scheme is one of the common names used to refer to Thailand’s Universal Coverage Scheme. Thai citizenship and Thai ID numbers are required to be eligible for this scheme.

Conclusion

Long-term visitors in Thailand will need comprehensive health insurance for their stay. If you want to make it easier on yourself, check out the health insurance options provided by Pacific Prime, since we offer plans with each of the above qualities that create a strong plan.

With over 25 years of reputation as a renowned health insurance broker, we tailor affordable, customized international health insurance plans that fit your needs and budgets. Compare quotes for free, or contact us today for a smooth transition to life as an expat in Thailand.

For some further reading, check out our articles about health insurance for tourists in Thailand and senior health insurance for expats in Thailand.

With his keen interest in journalism, especially in the healthcare and wellness field, Tawan joins Pacific Prime with the goal of creating content that simplifies health insurance solutions, helping people make informed choices and choose the best options for their needs. He firmly believes that words have power that can shape the world for the better.

- Cigna Global Health Insurance in Thailand for Expats - August 5, 2026

- Thailand Health Insurance For Long-Term Visitors - August 3, 2026

- UAE Family Health Insurance: Coverage for 2026 - May 28, 2026

Comments

2 Comments

How do expats in Thailand typically handle banking and financial matters, such as opening a bank account and transferring money internationally?

Expats in Thailand typically handle banking by opening a local bank account with institutions such as Bangkok Bank or Kasikorn Bank, which provide services tailored to foreigners, including English-speaking staff. For international money transfers, they often use online services like Wise or Revolut for lower fees and favorable exchange rates. To simplify the process, expats should prepare necessary documents, including a passport, visa, proof of address, and a letter of employment if required.

For more tailored financial advice or help navigating expat life in Thailand, contact us through the Contact Us page at Pacific Prime!

Ask a Question

We'll notify you

when our team replies!